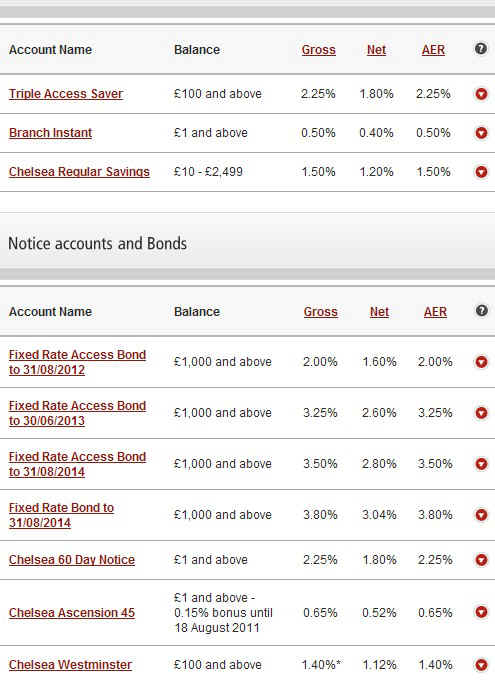

At first glance, the Chelsea website is an ancient design (see left) - you can expand out each account type but to obtain details (including the interest rate) you have to click on each of about 20 links. However, if you spot it on the left of the home page, there is a link to 'interest rates' - an all are displayed clearly as shown above. This is what most savers need.

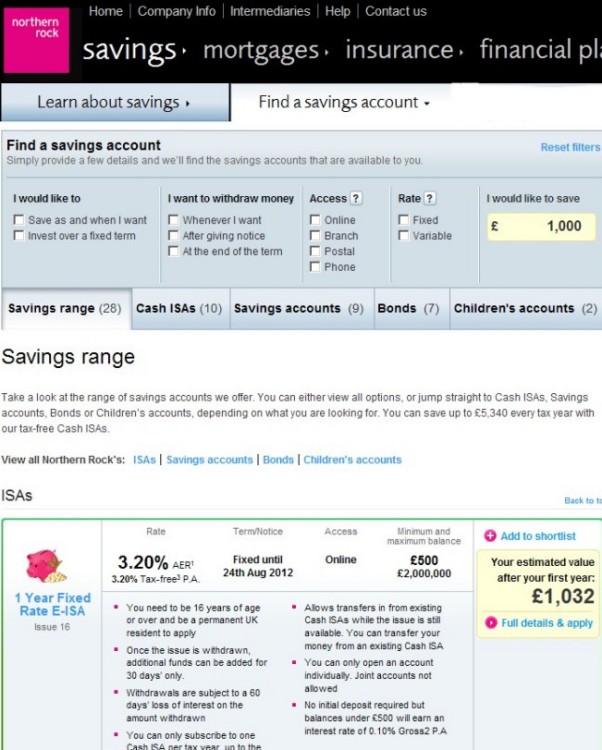

This approach gives users the option of selecting what type of account they wish to have (Branch/Postal/ISA etc) BEFORE they even know most of the interest rates. And it is the rate that may be the principal deciding factor. Some 'money comparison' websites also work in this way.

In effect you are invited to close off some of your options before you even know what you might be missing! And then if you think you might be, you go back to the beginning and start again.

You can scroll down a very long list of all account types (starting with ISAs as shown) but you'd need to make a list of the rates paid on each type of account as you went, and before it disappeared from view.

Applying the filters can also be unhelpful - selecting 'save as and when I want' produces 13 ordinary instant access and some ISA accounts - it is unlikely a customer wanting one type would be interested in another.

Technically, it all works very well and NR are very efficient on the phone.

It's an example of a highly developed and very artistic 'interactive' website - one whose developers may have lost sight of the fact that most people might like the simple option - some means of viewing 'at a glance' all the interest rates on one screen.

In some respects therefore, it is a little like the website of Sidmouth FolkWeek 2011.

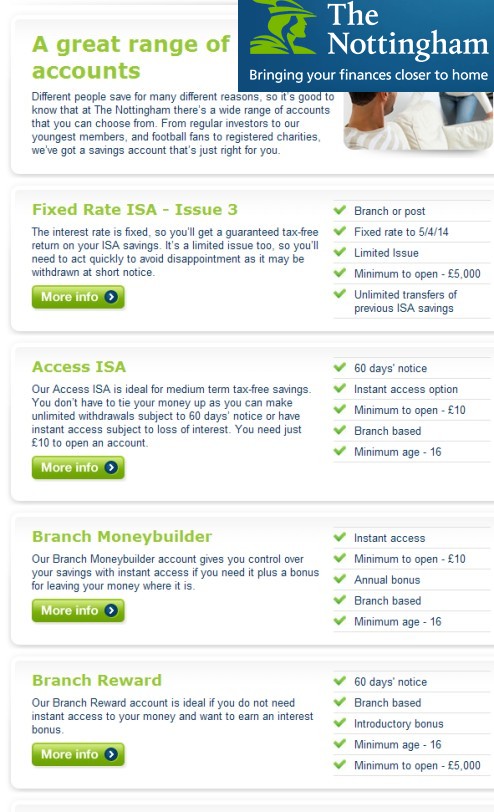

Amongst the types of presentation illustrated here, that from the Nottingham Building Society is perhaps one of the worst. But they are always efficient in operating their postal accounts and telephone service is good too - more than can be said of some other societies and banks.

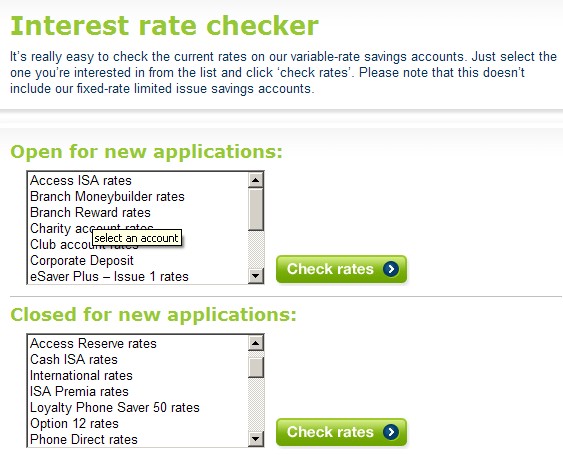

On the left is the main list of account types (a very long list that scrolls well off the top of the screen) and it gives you just about every detail of all the accounts on offer except the information you most need.

But there is an option to see all interest rates at a glance - but only if you first click on each and every account type! There is a further page "Pick the right savings account" this is very like the Northern Rock product selector where you are invited to close off options before you know what they offer.

Overall, it is all very artistic and interactive - and, arguably, as badly designed as the Sidmouth FolkWeek website in 2011.

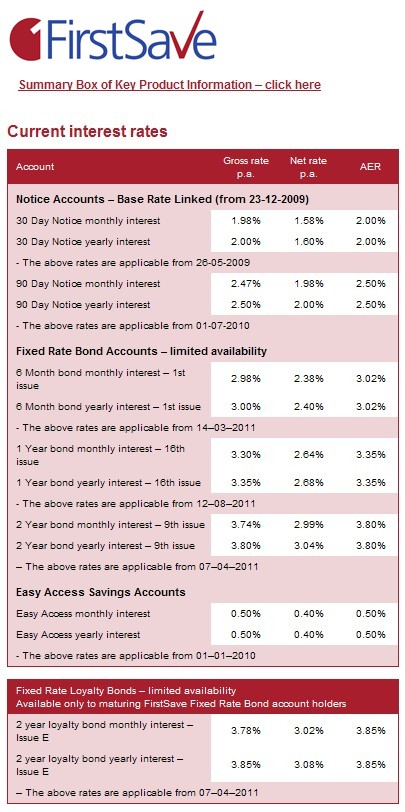

The customer service from FirstSave is first rate too.

Whilst their fixed rate bonds are often competitive, it can be seen at a glance that their instant access account would be best avoided.

At the time of this advert, it was possible to obtain 3% on an 'instant access' account from other providers.

What FirstSave do not do anywhere on their website is to state that FBN means First Bank of Nigeria - they are a UK based (and regulated) offshoot of a Nigerian bank. And given the number of 'scams' operated from that country it might put some people off investing.

But not to worry - they have full UK status and their customer service would put some UK and EU banks to shame. FBN in the UK operate from Newcastle Upon Tyne.

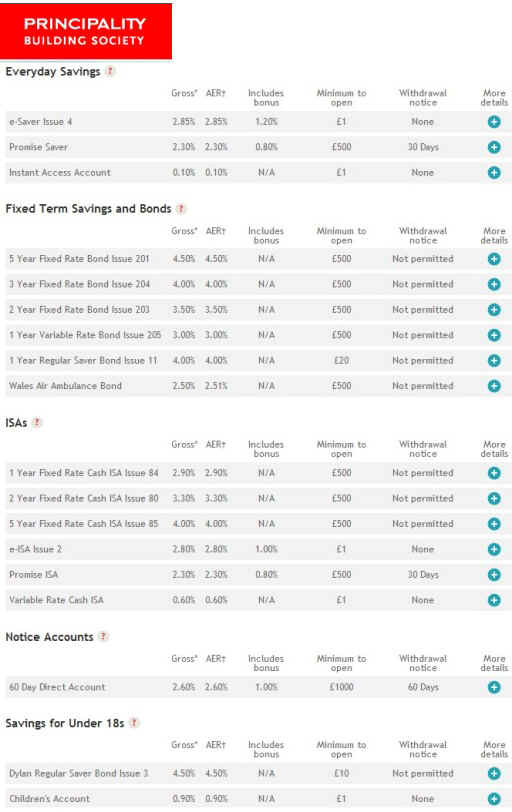

Another good example - and from one of the UK's smaller building societies, based in Wales.

This page lists many different account types and just manages to fit on a single screen. It is accessible in a single click from the home page. Another (and even more detailed) page listing interest rates is also available as a 'quick link' from the home page.

A good feature is that 'more details' about each account type can be obtained via the blue buttons - these produce a 'pop-up' box that leaves the main screen intact. It is very easy to use.

Who would bother with an instant access account at 0.10% when you could open an e-saver for Ł1 and enjoy 2.85%?

Yet people do - and it is the elderly who have no-one to help them who are increasingly disadvantaged by 'the digital divide'.

They are often the people who desperately need to earn as much interest as possible, yet lacking internet expertise they settle for the miserable rates on offer from local 'branch based' accounts.

Except in well-connected Sidmouth of course, where a friendly neighbour might help them.......